Business Is Back to Pre-Pandemic Levels for Home Remodeling Firms

With strong demand for their services, most firms have a positive outlook, the Q4 2020 Houzz Renovation Barometer shows

Erin Carlyle

October 19, 2020

Former Houzz Editorial Staff. Writing about the cost of renovation and what it takes to remodel. Former Forbes real estate reporter. Fascinated by cool homes, watching the bottom line.

Former Houzz Editorial Staff. Writing about the cost of renovation and what it takes... More

Business has recovered to pre-pandemic levels for design and construction firms in the residential remodeling industry, new data from Houzz shows. And the construction sector of the industry is reporting its strongest level of recent business activity since the third quarter of 2018.

“The results from the Houzz Q4 Barometer show that the home remodeling and design industry is truly resilient, and is seeing business activity return to pre-pandemic levels,” says Marine Sargsyan, Houzz senior economist.

“The results from the Houzz Q4 Barometer show that the home remodeling and design industry is truly resilient, and is seeing business activity return to pre-pandemic levels,” says Marine Sargsyan, Houzz senior economist.

The Q4 2020 Houzz Renovation Barometer looks at fourth-quarter residential renovation market expectations, project backlogs and recent business activity among firms in the construction and architectural and design services sectors, based on responses from 1,696 small businesses on Houzz. The survey was fielded Sept. 24 through Oct. 7.

“Home professionals have a positive outlook through the end of the year, despite unprecedented uncertainty due to the pandemic and the upcoming election, increasing supply chain constraints as well as shortages in the labor market,” Sargsyan says. “Pros are taking on new clients remotely using online tools and collaboration platforms, continuing the momentum from the recent quarter.”

An eventful year has pushed many firms to change the way they run their businesses. Architecture and design firms responded to pandemic-related business challenges by offering video consultations (56%), implementing safety guidelines at the office and project site (49%), providing remote collaboration tools (48%) and sourcing more products online (46%). Construction businesses implemented new safety guidelines (60%), used video consultation tools (33%) and sourced more products online (31%). Many of these solutions are supported by Houzz Pro business and project management software.

At the start of the fourth quarter of 2020, 85% of firms in the architectural and design services sector and 87% of firms in the construction sector have a neutral to very good outlook for the rest of the year, compared with 73% and 82%, respectively, at the start of the third quarter.

Read on to find out more about what remodeling industry firms said about current business conditions. We’ll look first at construction companies and then at firms in the architectural and design services areas. We’ll start with their business activity over the previous three months, then look at their project wait times, and lastly we’ll see what these firms expect for the next three months.

See how Houzz Pro can help your business with a 30-day free trial

“Home professionals have a positive outlook through the end of the year, despite unprecedented uncertainty due to the pandemic and the upcoming election, increasing supply chain constraints as well as shortages in the labor market,” Sargsyan says. “Pros are taking on new clients remotely using online tools and collaboration platforms, continuing the momentum from the recent quarter.”

An eventful year has pushed many firms to change the way they run their businesses. Architecture and design firms responded to pandemic-related business challenges by offering video consultations (56%), implementing safety guidelines at the office and project site (49%), providing remote collaboration tools (48%) and sourcing more products online (46%). Construction businesses implemented new safety guidelines (60%), used video consultation tools (33%) and sourced more products online (31%). Many of these solutions are supported by Houzz Pro business and project management software.

At the start of the fourth quarter of 2020, 85% of firms in the architectural and design services sector and 87% of firms in the construction sector have a neutral to very good outlook for the rest of the year, compared with 73% and 82%, respectively, at the start of the third quarter.

Read on to find out more about what remodeling industry firms said about current business conditions. We’ll look first at construction companies and then at firms in the architectural and design services areas. We’ll start with their business activity over the previous three months, then look at their project wait times, and lastly we’ll see what these firms expect for the next three months.

See how Houzz Pro can help your business with a 30-day free trial

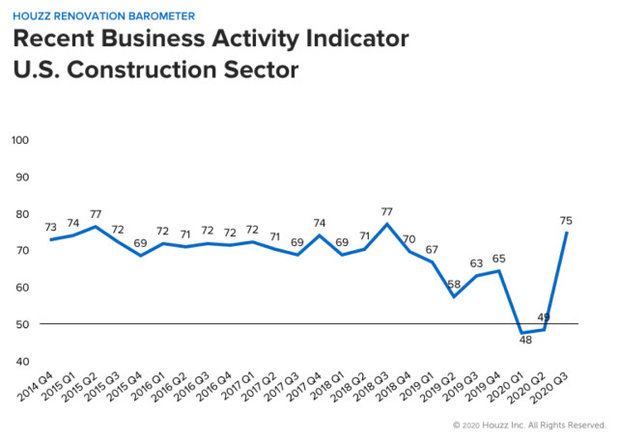

A score higher than 50 indicates that more firms reported increases than decreases in their recent business activity.

Construction Firms

1. Recent business activity increased significantly. An increase in new project inquiries and new committed projects in July, August and September lifted the Recent Business Activity Indicator of the Barometer to 75 for construction firms, up 26 points from the previous quarter. Construction firms have not seen a level of activity this strong in nearly two years, since third-quarter 2018.

Relative to a year ago, this indicator is up 12 points.

The Recent Business Activity Indicator looks at actual activity over the previous three months. In contrast with the Expected Business Activity and Project Backlog indicators (read more about these below), which look forward in time, the Recent Business Activity Indicator looks back. It’s based on survey questions that ask businesses to report whether they observed the actual number of project inquiries and new committed projects increasing, decreasing or staying the same in the previous three months relative to the three months before that. A score higher than 50 indicates that more firms reported increases than decreases.

Construction Firms

1. Recent business activity increased significantly. An increase in new project inquiries and new committed projects in July, August and September lifted the Recent Business Activity Indicator of the Barometer to 75 for construction firms, up 26 points from the previous quarter. Construction firms have not seen a level of activity this strong in nearly two years, since third-quarter 2018.

Relative to a year ago, this indicator is up 12 points.

The Recent Business Activity Indicator looks at actual activity over the previous three months. In contrast with the Expected Business Activity and Project Backlog indicators (read more about these below), which look forward in time, the Recent Business Activity Indicator looks back. It’s based on survey questions that ask businesses to report whether they observed the actual number of project inquiries and new committed projects increasing, decreasing or staying the same in the previous three months relative to the three months before that. A score higher than 50 indicates that more firms reported increases than decreases.

2. Project wait times rose nationally. With demand for their services strong, construction businesses that are focused on remodeling reported that wait times before they can take on a midsize project from a new client now average 7.2 weeks, up 1 week compared with the start of the previous quarter.

One year ago, the national average wait time was 5.2 weeks, meaning the average wait time has risen by 2 weeks year over year.

Among construction firms, build-only remodelers have the longest average wait time before they can take on a midsize project: 7.3 weeks, up 1.9 weeks from the start of the prior quarter. Wait times for design-build remodelers average 7.1 weeks, up 0.1 week compared with the start of the previous quarter.

One year ago, the national average wait time was 5.2 weeks, meaning the average wait time has risen by 2 weeks year over year.

Among construction firms, build-only remodelers have the longest average wait time before they can take on a midsize project: 7.3 weeks, up 1.9 weeks from the start of the prior quarter. Wait times for design-build remodelers average 7.1 weeks, up 0.1 week compared with the start of the previous quarter.

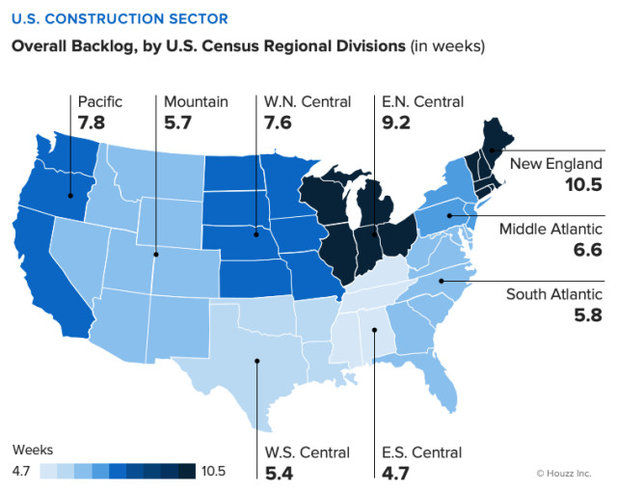

Backlogs range widely by region, as this map shows. The East South Central division of the U.S. (Alabama, Kentucky, Mississippi, Tennessee) has the shortest average wait time (4.7 weeks), while the New England division (Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont) has the longest (10.5 weeks) among the nine geographic divisions as defined by the U.S. Census.

See more resources for pros in Houzz Pro Learn

See more resources for pros in Houzz Pro Learn

A score higher than 50 indicates that more firms reported increases than decreases in their business expectations. Q2 2020 marked the first time since the Houzz Barometer began in 2015 that scores fell below 50.

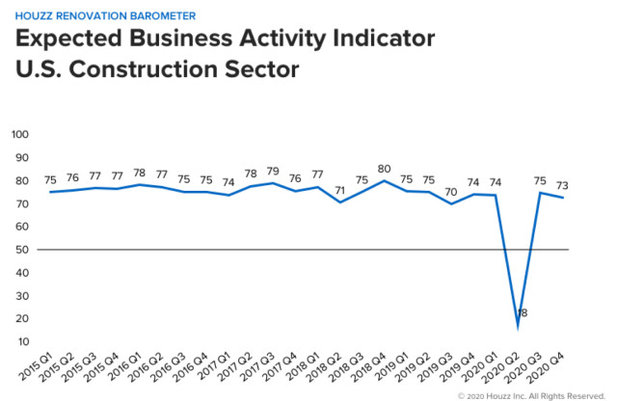

3. Expectations for business activity decreased slightly. After reporting strong expectations at the start of Q3, build-only remodelers and design-build remodelers reported slightly lowered expectations for business activity going into the fourth quarter of 2020. The Expected Business Activity Indicator decreased from 75 to 73 for Q4. Still, that level is significantly up from the all-time low of 18 seen at the start of the second quarter of this year, in the early days of the pandemic. It’s also about in line (just 1 point down) with expectations at the start of the year.

Compared with a year ago, the Expected Business Activity Indicator for construction firms is down 1 point.

The Expected Business Activity Indicator is based on survey questions that asked businesses to report whether they expected the number of project inquiries and new projects to increase, decrease or be unchanged in the coming three months compared with the prior three months. A score higher than 50 indicates that more firms expected increases than decreases.

3. Expectations for business activity decreased slightly. After reporting strong expectations at the start of Q3, build-only remodelers and design-build remodelers reported slightly lowered expectations for business activity going into the fourth quarter of 2020. The Expected Business Activity Indicator decreased from 75 to 73 for Q4. Still, that level is significantly up from the all-time low of 18 seen at the start of the second quarter of this year, in the early days of the pandemic. It’s also about in line (just 1 point down) with expectations at the start of the year.

Compared with a year ago, the Expected Business Activity Indicator for construction firms is down 1 point.

The Expected Business Activity Indicator is based on survey questions that asked businesses to report whether they expected the number of project inquiries and new projects to increase, decrease or be unchanged in the coming three months compared with the prior three months. A score higher than 50 indicates that more firms expected increases than decreases.

Architectural and Design Services Firms

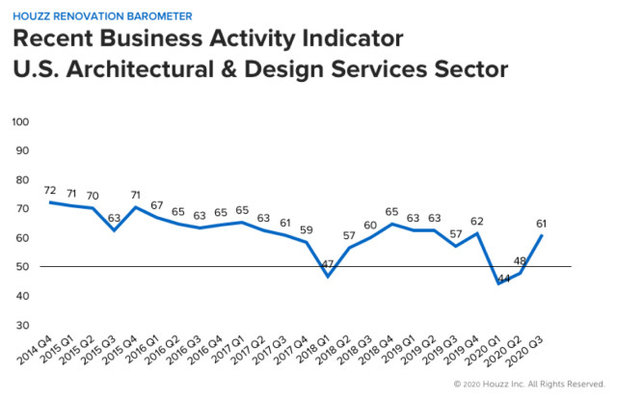

1. Recent business activity rose. Similar to construction firms, architecture and design firms welcomed an uptick in recent project inquiries and new committed projects in July, August and September. Their score for the Recent Business Activity Indicator of the Barometer increased to 61, a 13-point rise from the prior three months. Relative to the same period a year ago, this indicator is up 4 points.

1. Recent business activity rose. Similar to construction firms, architecture and design firms welcomed an uptick in recent project inquiries and new committed projects in July, August and September. Their score for the Recent Business Activity Indicator of the Barometer increased to 61, a 13-point rise from the prior three months. Relative to the same period a year ago, this indicator is up 4 points.

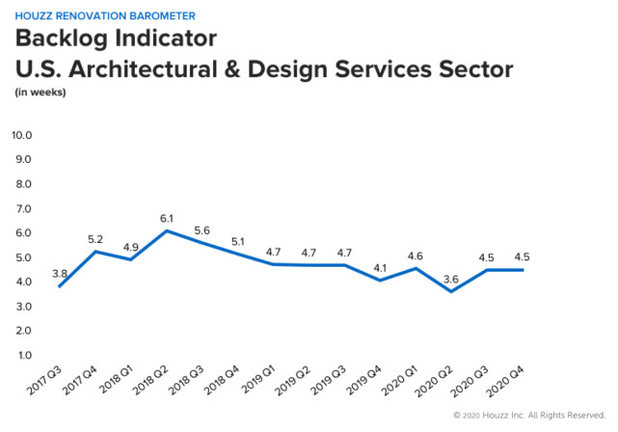

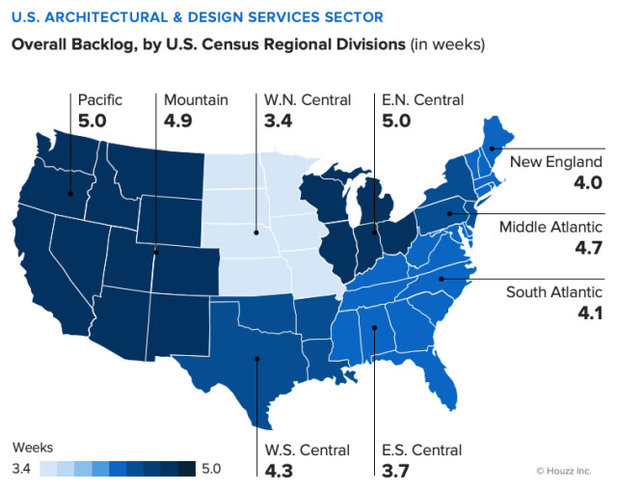

2. Wait times held steady nationally. The Project Backlog Indicator for architectural and design firms averages 4.5 weeks nationally at the start of the fourth quarter of 2020, flat with the start of Q3 2020.

Compared with a year ago, when wait times were 4.1 weeks, wait times are up 0.4 week.

Taking a closer look by professional type, interior designers have longer wait times to take on a new midsize project (4.8 weeks, up 2 weeks relative to the start of the previous three months) than do architects (4.3 weeks, down 1.2 weeks relative to the start of the previous three months).

Compared with a year ago, when wait times were 4.1 weeks, wait times are up 0.4 week.

Taking a closer look by professional type, interior designers have longer wait times to take on a new midsize project (4.8 weeks, up 2 weeks relative to the start of the previous three months) than do architects (4.3 weeks, down 1.2 weeks relative to the start of the previous three months).

Again, backlogs vary significantly by region, as this map shows. The West North Central division of the U.S. (Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, South Dakota) has the shortest average wait time (3.4 weeks), while the East North Central division (Illinois, Indiana, Michigan, Ohio, Wisconsin) and Pacific division (California, Oregon, Washington) have the longest (5 weeks).

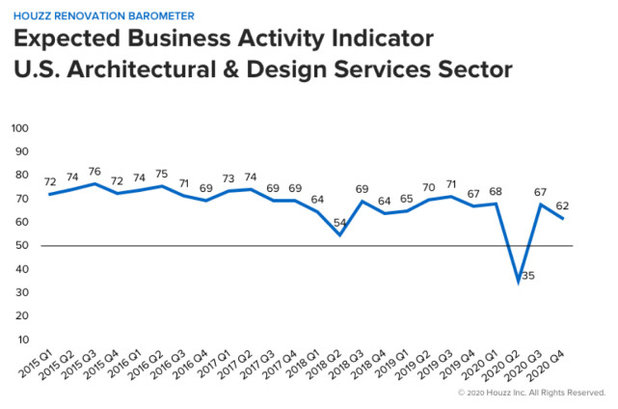

3. Business activity expectations decreased somewhat. Architects and interior designers reported moderately lowered expectations for new business activity for the fourth quarter of 2020 compared with the start of the previous quarter. Their score of 62 for the Expected Business Activity Indicator shows that more firms are expecting increases in new business activity than are expecting decreases. This measure is down 5 points from the start of Q3 2020, when it was 67.

This score is also down 5 points compared with the same period a year ago.

Architects reported a 7-point decrease in overall expectations, to 57, relative to the start of Q3 2020. Interior designers’ expectations decreased by 3 points, to 70, relative to the start of the third quarter.

This score is also down 5 points compared with the same period a year ago.

Architects reported a 7-point decrease in overall expectations, to 57, relative to the start of Q3 2020. Interior designers’ expectations decreased by 3 points, to 70, relative to the start of the third quarter.

The Houzz Renovation Barometer is based on a quarterly online survey sent to a national panel of U.S. businesses with profiles on Houzz. The Barometer includes three components: Expected Business Activity, Recent Business Activity and Project Backlog (or wait times). Expectations and business activity data are smoothed out to allow for predictable seasonal fluctuations, while wait-time data are not.

If you’re a pro and would like to offer your insights on market conditions in your area by joining the Barometer panel, please click here.

Read more on this and past Barometer reports

Tell us: Whether you’re a pro or a homeowner, we’d love to hear how this report compares with your experiences. Please share in the Comments.

More on Houzz

Read more stories about remodeling trends

Learn about Houzz Pro software

Talk with your peers in the Pro-to-Pro discussions

Join the Houzz Trade Program

If you’re a pro and would like to offer your insights on market conditions in your area by joining the Barometer panel, please click here.

Read more on this and past Barometer reports

Tell us: Whether you’re a pro or a homeowner, we’d love to hear how this report compares with your experiences. Please share in the Comments.

More on Houzz

Read more stories about remodeling trends

Learn about Houzz Pro software

Talk with your peers in the Pro-to-Pro discussions

Join the Houzz Trade Program

As a full-service, family-owned remodeling company in New Albany, OH, we strive to bring our clients incredible... Read More

What are you working on?

Related Products

Related Stories

Latest News for Professionals

Pros Remain Somewhat Optimistic Despite Slowed Activity

More construction and design firms expect business growth than expect a decline, the Houzz Q2 2024 Barometer shows

Full Story

Inside Houzz

Homeowners Spend More on Remodels Despite Slight Dip in Activity

Also, planning time far exceeds building time and pro hiring remains strong, the 2024 U.S. Houzz & Home Study reveals

Full Story

Kitchen Design

10 Top Kitchen Design Trends for Cabinets, Countertops and More

See the latest colors, styles and materials for popular kitchen features from the 2024 U.S. Houzz Kitchen Trends Study

Full Story

Kitchen Design

9 Kitchen Remodeling Trends Everyone Should Know About Now

See the latest on open floor plans, cabinet colors, pro hiring and more from the 2024 U.S. Houzz Kitchen Trends Study

Full Story

Latest News for Professionals

Outlook Is Mildly Optimistic Among Design and Construction Pros

Business activity and expectations grew, the Q1 2024 Houzz Renovation Barometer shows. Backlogs are at 2019 levels

Full Story

Latest News for Professionals

Business Outlook Diverges for Design and Construction Pros

See how expectations and project backlogs differ among remodeling sectors, per the Q4 2023 Houzz Renovation Barometer

Full Story

Bathroom Design

These Are the Bathroom Styles and Features Homeowners Want Now

See popular design ideas for colors, materials, vanity types and more, from the 2023 U.S. Houzz Bathroom Trends Study

Full Story

Bathroom Design

6 Bathroom Remodeling Trends Everyone Should Know About

Learn about big-picture design and renovation activity happening now, from the 2023 U.S. Houzz Bathroom Trends Study

Full Story

Inside Houzz

15% of Homeowners Are Postponing Home Improvement Projects

But more than half have a project in the works or plan to start one by the end of 2024, according to a new Houzz survey

Full Story

Latest News for Professionals

Pros Are Mildly Optimistic Despite Slowed Activity in Q2 2023

Expectations are restrained and construction pros report record-high backlogs in the Q3 2023 Houzz Renovation Barometer

Full Story

Thank you Erin for the great article! We have seen a surge of business right after Michigan opened back up in May. It's been going strong but has slowed a little in the past few weeks but we see this every election year. Once the election is over things will pick back up. I think the shutdown and shelter in place has given many homeowners the chance to actually lived in their houses and see the condition it's in. So many homeowners are gone all day working then running around after work and on weekends that they don't really stop and see how much they need to work on the house.

We all hope to get through this pandemic safely and return to normal life but that may be a while so everyone stay safe and stay positive!

~Nicole

Hello all, I am an interior designer working in a Dallas tile showroom right now and when I ask the designers, builders, etc. I f they are busy most will say they have never been busier. Most have five or more project going on and the larger firms will have several. Our biggest dilemma is getting product. The tariffs last fall and winter started a shift of production out of China as product increased in price, sometimes by 200%. Then as production was coming on line in India, Turkey, Portugal, Brazil, and so on, Covid hit and production was shut down. Once a product it produced it must get to the ocean dock, then travel up to 45 days to get to a US port, then customs and then who knows how long to transport to distribution centers. I have lost a few thousand in sales because product is simply not available in a reasonable amount of time for clients. If you like it, order it and store it until you need it.