Comments

6 Takeaways From the Remodeling Industry in Early 2019

The Q1 Houzz Renovation Barometer reveals mixed expectations by U.S. firms for their business activity this quarter

Erin Carlyle

January 10, 2019

Former Houzz Editorial Staff. Writing about the cost of renovation and what it takes to remodel. Former Forbes real estate reporter. Fascinated by cool homes, watching the bottom line.

Former Houzz Editorial Staff. Writing about the cost of renovation and what it takes... More

Residential remodeling industry firms have mixed expectations for their businesses for the first three months of 2019, new data from Houzz reveal. Those on the construction side express new caution, while architectural and design firms report a boost in new business activity.

As a remodeling professional, your business is closely tied to what’s happening for other pros. So it can be helpful for design firms to know what construction firms are reporting and vice versa. The Q1 2019 Houzz Renovation Barometer tracks residential renovation market expectations, project wait times and recent business activity based on responses from more than 2,200 small businesses on Houzz. Read on for a picture of the remodeling industry, straight from firms in the trenches. We’ll start with construction firms and then move on to those in the architectural and design services areas.

As a remodeling professional, your business is closely tied to what’s happening for other pros. So it can be helpful for design firms to know what construction firms are reporting and vice versa. The Q1 2019 Houzz Renovation Barometer tracks residential renovation market expectations, project wait times and recent business activity based on responses from more than 2,200 small businesses on Houzz. Read on for a picture of the remodeling industry, straight from firms in the trenches. We’ll start with construction firms and then move on to those in the architectural and design services areas.

“Current Barometer readings and qualitative feedback reflect a mixed degree of caution about market conditions among contractors, architects and designers,” says Nino Sitchinava, principal economist at Houzz. Businesses are overwhelmingly concerned about rising costs of products and materials, as well as customers’ hesitance to start new projects given these rising costs, the survey reveals.

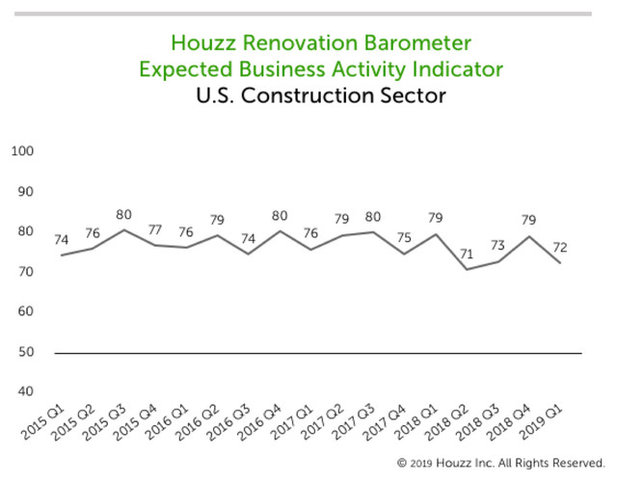

1. Construction Firms’ Business Activity Expectations Are Positive but Softened

Build-only remodelers, design-and-build remodelers and specialty trade contractors working on upgrades to existing homes anticipate an uptick in new projects, as well as inquiries from would-be clients about new projects for the first three months of 2019.

However, firms report less overall positivity about business activity than they did in the last three months of 2018 — or for the same time frame one year ago. The Expected Business Activity Indicator (one component of the Barometer) decreased 7 points to 72 for the first three months of the year for construction firms. Relative to a year ago, this indicator is also down 7 points.

The Expected Business Activity Indicator is based on survey questions that asked businesses to report whether they expect the number of project inquiries and new projects to increase, decrease or be unchanged in the coming three months compared with the prior three months. A score higher than 50 indicates that more firms reported increases than decreases.

Build-only remodelers, design-and-build remodelers and specialty trade contractors working on upgrades to existing homes anticipate an uptick in new projects, as well as inquiries from would-be clients about new projects for the first three months of 2019.

However, firms report less overall positivity about business activity than they did in the last three months of 2018 — or for the same time frame one year ago. The Expected Business Activity Indicator (one component of the Barometer) decreased 7 points to 72 for the first three months of the year for construction firms. Relative to a year ago, this indicator is also down 7 points.

The Expected Business Activity Indicator is based on survey questions that asked businesses to report whether they expect the number of project inquiries and new projects to increase, decrease or be unchanged in the coming three months compared with the prior three months. A score higher than 50 indicates that more firms reported increases than decreases.

2. Client Wait Times for Construction Firms Have Decreased Nationally

Construction businesses focused on remodeling reported that wait times before they can take on a midsize project from a new client are now nearly two weeks shorter than a year ago — indicating a significant drop in the project backlogs facing construction firms. Wait times are now 4.8 weeks, compared with 6.5 weeks a year ago — a 1.7-week drop. Given this dramatic change, it’s no wonder that firms in the construction sector have softened their expectations for business activity for the first three months of the year.

However, expected wait times in the first quarter of 2019 rose compared with fourth-quarter 2018. This is to be expected due to both the winter holidays and seasonal weather patterns, since activity declines for the final three months of the year and then gets back on track in the new year. Expected wait times are now 4.8 weeks nationally for the first three months of 2019, up from 4.5 weeks at the end of last year, according to the Barometer’s Backlog Indicator for this group.

Among the construction firms, build-only remodelers have the longest average wait times before they can take on a midsize project: 7.5 weeks, up 0.7 weeks over the previous three months. Specialty trade contractors, such as those that do masonry, painting or electrical work, have the shortest project wait times at 3.1 weeks. Wait times for design-and-build remodelers are six weeks.

Read about regional variations in project wait times

Construction businesses focused on remodeling reported that wait times before they can take on a midsize project from a new client are now nearly two weeks shorter than a year ago — indicating a significant drop in the project backlogs facing construction firms. Wait times are now 4.8 weeks, compared with 6.5 weeks a year ago — a 1.7-week drop. Given this dramatic change, it’s no wonder that firms in the construction sector have softened their expectations for business activity for the first three months of the year.

However, expected wait times in the first quarter of 2019 rose compared with fourth-quarter 2018. This is to be expected due to both the winter holidays and seasonal weather patterns, since activity declines for the final three months of the year and then gets back on track in the new year. Expected wait times are now 4.8 weeks nationally for the first three months of 2019, up from 4.5 weeks at the end of last year, according to the Barometer’s Backlog Indicator for this group.

Among the construction firms, build-only remodelers have the longest average wait times before they can take on a midsize project: 7.5 weeks, up 0.7 weeks over the previous three months. Specialty trade contractors, such as those that do masonry, painting or electrical work, have the shortest project wait times at 3.1 weeks. Wait times for design-and-build remodelers are six weeks.

Read about regional variations in project wait times

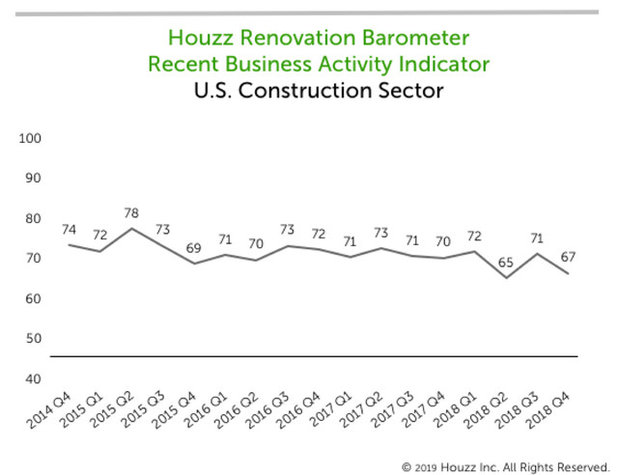

3. Recent Business Activity Drops for Construction Firms

A drop in new-project inquiries and new projects in October, November and December pushed the Recent Business Activity component of the Barometer to 67 for construction firms, down 4 points compared with the prior three months. Relative to the same period a year earlier, this indicator is down 3 points.

The Recent Business Activity component looks at actual activity over the past three months. (In contrast with the Expected Business Activity and Project Backlog indicators, which look forward in time, the Recent Business Activity Indicator looks back in time.) It is based on survey questions that ask businesses to report whether they observed the actual number of project inquiries and new projects increasing, decreasing or staying the same in the past three months relative to the prior three months. Recent Business Activity Indicator scores can be compared with the Expected Business Activity Indicator scores for any given three-month period or quarter to see whether actual activity met, exceeded or fell short of expectations.

“It is notable that, relative to a year ago, expectations and recent activity among contractors are more subdued and project backlogs are considerably lighter,” Sitchinava says.

A drop in new-project inquiries and new projects in October, November and December pushed the Recent Business Activity component of the Barometer to 67 for construction firms, down 4 points compared with the prior three months. Relative to the same period a year earlier, this indicator is down 3 points.

The Recent Business Activity component looks at actual activity over the past three months. (In contrast with the Expected Business Activity and Project Backlog indicators, which look forward in time, the Recent Business Activity Indicator looks back in time.) It is based on survey questions that ask businesses to report whether they observed the actual number of project inquiries and new projects increasing, decreasing or staying the same in the past three months relative to the prior three months. Recent Business Activity Indicator scores can be compared with the Expected Business Activity Indicator scores for any given three-month period or quarter to see whether actual activity met, exceeded or fell short of expectations.

“It is notable that, relative to a year ago, expectations and recent activity among contractors are more subdued and project backlogs are considerably lighter,” Sitchinava says.

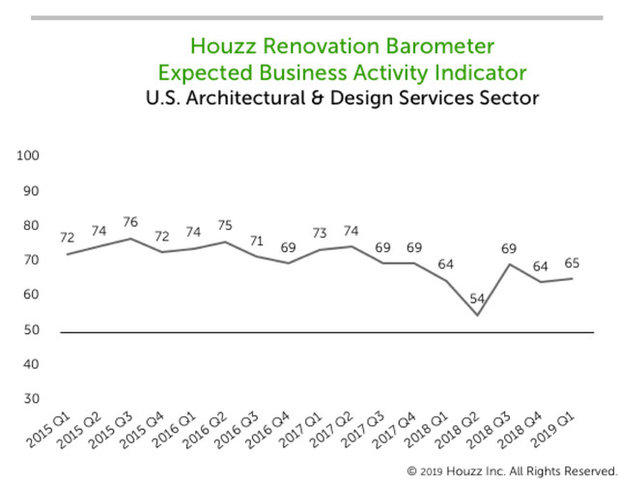

4. Architectural and Design Services Firms Expect Steady Positive Business Activity

Like construction firms, architects and interior designers expect renovation business activity to rise during the first three months of the year over the fourth quarter of 2018. However, this side of the industry has not seen a softening of expectations. “The sentiments and backlogs of architects and designers are on par with a year ago, likely explained by a boost in new business activity in the last quarter of 2018,” Sitchinava says.

Their score of 65 for the Expected Business Activity Indicator shows that there are more firms that anticipate increases than those that anticipate decreases. This score is up 1 point from the final three months of 2018, as well as up 1 point from the same period a year ago.

In general, the expectations of architectural and design firms tend to be more subdued compared with those of construction firms. The scores for the Expected Business Activity Indicator this quarter — 72 for construction firms, 65 for architectural and design firms — continue that trend.

Like construction firms, architects and interior designers expect renovation business activity to rise during the first three months of the year over the fourth quarter of 2018. However, this side of the industry has not seen a softening of expectations. “The sentiments and backlogs of architects and designers are on par with a year ago, likely explained by a boost in new business activity in the last quarter of 2018,” Sitchinava says.

Their score of 65 for the Expected Business Activity Indicator shows that there are more firms that anticipate increases than those that anticipate decreases. This score is up 1 point from the final three months of 2018, as well as up 1 point from the same period a year ago.

In general, the expectations of architectural and design firms tend to be more subdued compared with those of construction firms. The scores for the Expected Business Activity Indicator this quarter — 72 for construction firms, 65 for architectural and design firms — continue that trend.

5. Wait Times for Architectural and Design Services Firms Are Down Nationally

The Backlog Indicator for architectural and design firms fell to an average of 4.7 weeks nationally for the first three months of the year. That is a decrease of 0.4 weeks compared with the last three months of 2018 and a drop of 0.2 weeks compared with the first quarter of 2018. Architects and interior designers currently have similar wait times to take on a new midsize project: 4.7 weeks and 4.8 weeks, respectively.

The Backlog Indicator for architectural and design firms fell to an average of 4.7 weeks nationally for the first three months of the year. That is a decrease of 0.4 weeks compared with the last three months of 2018 and a drop of 0.2 weeks compared with the first quarter of 2018. Architects and interior designers currently have similar wait times to take on a new midsize project: 4.7 weeks and 4.8 weeks, respectively.

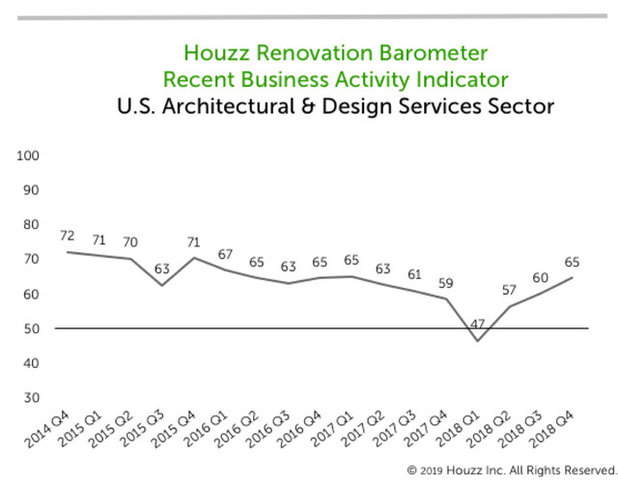

6. Recent Business Activity Up for Architectural and Design Services Firms

Architectural and design services businesses reported that new projects and new-project inquiries rose from October through December. The Recent Business Activity Indicator for this sector rose to 65, a 5-point increase over the score for June, July and August. The indicator for fourth-quarter 2018 is up 6 points compared with the fourth quarter of 2017.

Architectural and design services businesses reported that new projects and new-project inquiries rose from October through December. The Recent Business Activity Indicator for this sector rose to 65, a 5-point increase over the score for June, July and August. The indicator for fourth-quarter 2018 is up 6 points compared with the fourth quarter of 2017.

The Houzz Renovation Barometer is based on a quarterly online survey sent to a national panel of U.S. businesses with a profile on Houzz. The Barometer includes three components: expected business activity, recent activity and backlogs (or wait times). Expectations and business activity data are smoothed out to allow for predictable seasonal fluctuations, while wait-time data are not.

The Q1 2019 Houzz Renovation Barometer garnered responses from 2,270 firms and was fielded from Dec. 27, 2018, through Jan. 9, 2019.

If you would like to offer your insights on market conditions in your area by joining the Barometer panel, please click here.

Tell us: How does this survey compare with your firm’s experience? Share your thoughts in the Comments.

Read more Barometer reports

The Q1 2019 Houzz Renovation Barometer garnered responses from 2,270 firms and was fielded from Dec. 27, 2018, through Jan. 9, 2019.

If you would like to offer your insights on market conditions in your area by joining the Barometer panel, please click here.

Tell us: How does this survey compare with your firm’s experience? Share your thoughts in the Comments.

Read more Barometer reports

Related Products

Related Stories

Latest News for Professionals

Builders Share Ways Designers Can Help Them Deliver Great Work

Contractors on Houzz offer tips on how architects and interior designers can help residential projects run smoothly

Full Story

Industry Research

Pros Remain Somewhat Optimistic Despite Slowed Activity

More construction and design firms expect business growth than expect a decline, the Houzz Q2 2024 Barometer shows

Full Story

Latest News for Professionals

Designers Share 4 Ways Builders Can Help Deliver Great Work

Architects and interior designers on Houzz offer tips on how contractors can help residential projects run smoothly

Full Story

Latest News for Professionals

10 Spring Home Upgrades to Recommend to Your Clients Now

Boost business and customer confidence by suggesting home improvements that are tailored to the season

Full Story

Latest News for Professionals

Outdoor Flooring, Turf and Tile Products for 2024

By Julie Sheer

See the latest materials for patios, decks and yards on display at the recent Surfaces trade show

Full Story

Latest News for Professionals

Homeowners Spend More on Remodels Despite Slight Dip in Activity

Also, planning time far exceeds building time and pro hiring remains strong, the 2024 U.S. Houzz & Home Study reveals

Full Story

Latest News for Professionals

6 Pros Share the Time-Saving Practices They Rely On

Want to be more efficient with your time? Pros reveal the indispensable methods and tools they turn to again and again

Full Story

Latest News for Professionals

Design Pros Share 10 Favorite Creamy White Paints

By Becky Harris

These off-white color choices include versatile tones, warming hues and pleasingly soft shades

Full Story

Latest News for Professionals

5 Fresh Laundry Appliance Trends for 2024

Check out the lean, green, powerful and smart washers and dryers showcased at the KBIS 2024 trade event

Full Story

Latest News for Professionals

5 Trends in New Engineered Countertops and Surfaces for 2024

See the latest styles and features for quartz, porcelain and sintered stone showcased at the recent KBIS 2024 trade show

Full Story